The Determinants of Bank Service Quality in the Banking Sector of Botswana

Wilbert Kudakwashe Chidaushe*  , Stegi Shine and Mini Sebastian

, Stegi Shine and Mini Sebastian

1Department of Accounting and Finance, Botho University, Gaborone, Botswana .

wilbert.chidaushe@bothouniversity.ac.bw

http://dx.doi.org/10.12944/JBSFM.07.01.08

The study explored the determinants of bank service quality in the banking sector of Botswana. 800 respondents from commercial banks of Botswana were randomly served with the survey questionnaires. The study was based on quantitative research involving testing of the hypothesis. The data collected from the survey was subjected to confirmatory factor analysis and reliability analysis prior to running Structural Equation Modelling. The results of testing the hypothesis revealed that banking service quality is significantly and positively correlated with service characteristics of tangibles, responsiveness, assurance and empathy. Inconclusive evidence was obtained concerning the relationship between bank service quality and service characteristics of reliability. The study inverted a new Structural Equation Model A that balances theory and data collected in this study. The study hereby recommends bank managers to take proactive action towards significant improvement of appealing tangible bank processes and systems, providing inevitable assurance, responsiveness and empathy as well as consistently applying reliability to all its services characteristics. In addition, policy makers should strive to enact legislation that ensure that banking institutions provide services that strongly encourage sustainable economic development. The limitation of the study is that the results can not be replicated to other areas as the research focused entirely on the banking sector of Botswana.

Copy the following to cite this article:

Chidaushe W. K, Shine S, Sebastian M. âThe Determinants of Bank Service Quality in the Banking Sector of Botswanaâ. Journal of Business Strategy Finance and Management, 7(1).

DOI:http://dx.doi.org/10.12944/JBSFM.07.01.08Copy the following to cite this URL:

Chidaushe W. K, Shine S, Sebastian M. âThe Determinants of Bank Service Quality in the Banking Sector of Botswanaâ. Journal of Business Strategy Finance and Management, 7(1). Available here:https://bit.ly/3YJI7tr

Download article (pdf) Citation Manager Publish History

Introduction

The research examined the variables that affected the quality of bank services in Botswana's banking industry. The study concentrated on commercial banks and other private banks that are part of Botswana's banking sector. Providing high-quality banking services promotes both economic growth and social welfare.

The level of satisfaction of bank customers depends on the level of bank service quality delivered to them by the individual banks through their various systems, processes and activities. Parasuraman & Zeithami, and Berry (1988) divided the characteristics of service quality into the following categories: reliability, empathy, responsiveness, assurance and tangibles.

Desklib (2021) stressed that quality of the service, waiting and the customer complaint management are vital for a bank in the attainment of sustainable competitive position. The study was based on an empirical evaluation on how service quality dimensions impact customer satisfaction in the banking sector.

Research Gap

Anecdotal literature on the correlation between banks service quality with SERVQUAL characteristics of the tangibles, responsiveness, reliability, assurance and empathy lacks empirical evidence with Sub-Saharan examples but is abundant with Western, Latin America and Asian world cases (Dongol and Khadka, 2024; Ifedi et al., 2024: Wang et al.,2023: Thao, 2022; Zhou et al., 2021; Islam et al., 2021; Suzan et al., 2021 and Monosimanegape et al., 2020).. Therefore this research sought to close that gap.

Problem Statement

Provision of excellent service in the banking sector of Botswana remains an extreme challenge that is worthy to be addressed as the banking sector of Botswana is a major contributor to the GDP of the country. The banks in Botswana are frequently the subject of negative comments and criticism regarding formation of long queues, high bank charges and lack of banking services in the rural areas (Jefferis, 2015). Thus, this study looked at the variables that influence the quality of bank services in Gaborone's banking industry.

Research Questions

The following comprise the study's research questions:

What factors influence service quality in Botswana's banking industry?

How do certain service features provided by banks in Botswana relate to the quality of bank services?

Research Objectives

The study's objectives were to:

Analyze the factors that influence service quality in Botswana's banking industry and

Examine the connection between certain service attributes provided by banks and service quality.

The research hypothesis

The null hypothesis for the study was:

H0: Bank Service Quality is not significantly and positively correlated with service characteristics of the tangibles, empathy, assurance, responsiveness and reliability.

The alternative hypothesis for the study was that:

H1: Bank Service Quality is significantly and positively correlated with service characteristics of empathy, assurance, responsiveness, reliability and tangibles.

Materials and Methods

The goals of the study, which focuses on the factors that influence service quality and the connections between bank service quality and service quality dimensions, form the basis of the empirical review under this part.

According to Ifedi et al. (2024), consumer happiness is unaffected by tangibles or empathy. The survey also discovered that Malaysian banks' customer satisfaction is impacted by responsiveness, assurance, and dependability. The study used multiple regression analysis to test the hypothesis based on the social package for social sciences (SPSS) and was based on a sample of 317 respondents who were customers of Malaysian banks. Data for the study was gathered using structured questionnaires.

According to Awara et al. (2022), customer satisfaction is significantly impacted by the combined effects of the service quality elements of customer friendliness, bank automation efficacy, service attractiveness, and secure transactions. A sample of 947 respondents who were commercial bank clients served as the basis for the study. Cross-sectional surveys and phenomenological research served as the foundation for this study's research designs.

Neupane (2019) asserted that banks should focus more on the improvement of the tangibles, responsiveness and assurance. The study was based on a sample of 150 respondents of the public bank of Nepal and adopted a quantitative research design. The statistical tools used were the correlation and regression analysis based on stastical package for social science (SPSS).

Chiguvi et al. (2025) revealed a profound and positive correlation between bank customer satisfaction and bank customer experience enhanced by technological advancement and innovation in the banking sector of Botswana. The study underscored the importance of effectively managing customer experience leading to bank customer loyalty. The study was based on quantitative research and deployed descriptive statistics and applied regression analysis to examine the relationship between bank customer satisfaction and bank customer experience.

Wang et al. (2023) found that while accessibility and empathy had little impact on customer satisfaction for Bangladesh's non-banking financial institutions, assurance, dependability, responsiveness, and tangibility had a substantial impact. The SERVPERF model served as the foundation for the investigation, which used partial least square structural equation modeling.

According to Lim et al. (2023), client satisfaction with e-banking services was significantly influenced by website design, security or privacy, timeliness, and dependability. A sample of 138 respondents served as the basis for the investigation. Partial least squares and SPSS were used in the study to process the data.

Chiguvi (2023) observed a positive and profound relationship between ABSA Bank's tangibles, responsiveness, assurance, empathy, and responsiveness with the quality of its bank services. The study used a sample of 180 ABSA Bank clients and was based on qualitative descriptive research.

Dongol and Khadka (2024) found that in Nepal's banking industry, tangibles, responsiveness, and empathy had a large and beneficial impact on customer satisfaction. Descriptive statistics, regression analysis, and Pearson correlation analysis served as the study's foundation. Twenty banks in the city of Kathmandu served as the study's sample. The study suggested that banks should increase the quality of their services in order to become more competitive.

According to Famiyeh et al. (2018), customer satisfaction for banks was significantly correlated with ambience, social elements, and dependability. Bank customer satisfaction was not significantly correlated with assurance or responsiveness. Additionally, the study found a direct and positive correlation between client loyalty and customer satisfaction. The study used partial least squared structural equation modeling (PLS-SEM) and was based on a survey of the banking industry in Ghana.

According to Gonu et al. (2023), a significant predictor of customer happiness is customer orientation. A sample of 391 commercial bank clients from emerging nations served as the basis for the study. The study used a descriptive research approach and was quantitative in nature. Partial least squares structural equation modeling was used in the investigation.

According to Madhushani et al. (2023), customer satisfaction was substantially correlated with each of the five aspects of service qualityâtangible, responsiveness, empathy, assurance, and reliability. The study used a deductive research methodology with a sample of 400 respondents drawn from Sri Lankan banks using simple random selection. During the pandemic,

Bala et al. (2021) found a correlation between the loyalty and customer satisfaction of various mobile banking user categories. The survey, which focused on Bangladeshi rural residents, involved 180 respondents. The study's conclusions showed that during the COVID-19 lockdown, consumer satisfaction was significantly impacted by the mobile banking service's timeliness, efficiency, and dependability.

According to Mukelabai and Mulungu (2024), the two most significant aspects of quality that affected the perception of customer satisfaction at Stanbic Bank in Botswana were tangibility and assurance. The study came to the conclusion that the bank's level of service quality affected both client happiness and loyalty. To increase client happiness, it was suggested that banks concentrate on enhancing their responsiveness, empathy, and dependability. A sample of 340 respondents and 20 participants in in-depth interviews comprised the mixed-method research that served as the study's foundation.

According to Alall (2024), consumer satisfaction and the caliber of banking services are positively and significantly correlated. Based on a sample of 139 distinct banks, the study used STRATA to analyze its findings. Purposive selection of South Asian nations served as the study's foundation.

According to Feng et al. (2021), cloud services, security, e-learning, and service quality are the four elements that can influence a customer's satisfaction with online banking. According to the findings, there are four key elements that affect how satisfied customers are with Internet banking services: cloud services, security, e-learning, and service quality. The validity and reliability of the measurement model and the causal model were assessed in this study using the structural equation modeling method.

Muchimba and Sinkala (2024) discovered that whereas tangible features have little to no effect on customer satisfaction, banks' responsiveness, correctness, dependability, and empathy had a considerable impact. To boost client happiness, the survey advised banks to put more of an emphasis on responsiveness, security, empathy, and dependability. Based on a sample of 397 Zanaco Bank respondents, the study used a descriptive causal design and analyzed the data using Spearman's correlation.

Thao (2022) found that customer satisfaction and bank service quality were directly correlated. Furthermore, the study demonstrated a favorable correlation between customer satisfaction and the way in which customers perceived the service product, the human element of service delivery, and the process element of service delivery. A survey with a random selection of Vietnibank employees in Vietnam served as the basis for the study. For the study, a quantitative research methodology was chosen. In the study, analysis of variance (ANOVA) was employed.

Tedjokusumo and Murhadi (2023) discovered that while the privacy and security variable had no discernible effect on customer satisfaction, the reliability, customer service and support, and responsiveness variables significantly increased customer satisfaction. Customer loyalty was also found to be significantly positively impacted by customer satisfaction. Purposive sampling was employed to pick the survey's 194 respondents, which served as the basis for the study.

For both Indian and Pakistani banks, Patel et al. (2023) found a generally substantial positive correlation between e-loyalty, e-satisfaction, and e-service quality. A sample of 400 Indian and Pakistani users of online banking services served as the basis for the study. Partial least square structural equation modeling was used to analyze the study.

According to Siregar and Kusumawati (2023), customer satisfaction was positively impacted by Bank Jago's service quality, which included responsiveness, efficiency, site organization, and user friendliness. Furthermore, the study found that among Bank Jago customers, customer loyalty was positively impacted by customer satisfaction. The study's methodology was quantitative, and its findings were analyzed using partial least square structural equation modeling and descriptive statistics. A sample of 318 respondents from the Bank of Jago served as the basis for the study, which used the purposive sampling approach to choose its participants.

The significance of system quality, interface design, service quality, and security assurance in relation to mobile banking loyalty intention was emphasized by Zhou et al. (2021). Structural equation modeling (SEM) was used to assess the study, which was based on a survey of 224 mobile bank customers.

Christanto and Santoso (2022) demonstrated that customer satisfaction was positively and significantly impacted by the variables of service quality and business image. The study also showed that customer loyalty was positively and significantly impacted by customer satisfaction. A survey of 200 Indonesian bank clients served as the basis for the study.

Singh (2019) found that customer satisfaction with online banking was positively and significantly correlated with responsiveness, efficiency, and perceived credibility. A poll of 650 Indian respondents served as the basis for the study. Sampling appropriateness for the study was evaluated using exploratory and confirmatory factor analysis. The association between internet banking customer happiness and quality factors was examined using multi regression analysis.

Islam et al. (2021) discovered a strong and positive correlation between visibility, employee dedication, responsiveness, and customer satisfaction. The study also demonstrated a negligible association between reliability, access, and customer satisfaction in Bangladesh's private banking sector. Furthermore, the study uncovered a positive and profound association between customer satisfaction and customer loyalty. The study was based on quantitative research that used structural equation modelling to test the hypothesis. The study's sample size was 200 self-administered questionnaires from Bangladesh's private banking sector.

Suzan et al. (2021) stressed that the factors that determine a bank's performance are tangibles, assurance, responsiveness, and dependability. Descriptive research served as the foundation for the study, which also included hypothesis testing. Using SPSS, various regression tests were performed on 445 questionnaires given to Asian bank customers.

Monosimanegape et al. (2020) found a link between the quality service dimension of assurance, responsiveness, tangibles, responsiveness, empathy and service quality of the public sector of Botswana. Descriptive inferential statistics was deployed in processing the data of the research. The sample size of 135 was extracted for the study from Botswana's Tonota Sub Region.

According to Raza et al. (2020), customer satisfaction had a strong and positive correlation with customer loyalty, and all quality characteristics had a strong and positive correlation with customer satisfaction. A sample of 500 bank clients in Pakistan were given standardized questionnaires as the basis for this quantitative investigation. Partial least squares structural equation modeling was used in the investigation.

According to Vinnarasi et al. (2022), there is a connection between customer satisfaction and service quality. The study also found that the dynamics of the banking business had changed as a result of consumer satisfaction. Mono qualitative secondary empirical data served as the study's foundation.

Das and Jannat (2018) discovered that state-owned commercial banks in Bangladesh do not provide satisfactory customer service. The survey also showed that customers' perceptions were significantly and favorably impacted by civility, staff appearance, transaction safety and correctness, and service reliability. The study also found that customer satisfaction was negatively impacted by rapid service and individualized attention to customers. The survey came to the conclusion that among the aspects of bank quality, clients place a higher value on the tangibles, assurance, and dependability of the bank's services.

Khan et al. (2018) discovered a strong and favorable correlation between the dimensions of assurance, tangibility, responsiveness, empathy, and dependability with customer satisfaction. Partial least square structured regression modeling was used in the study, which was based on a survey of 240 respondents. The study's respondents were chosen using a convenience sample technique.

In Botswana's banking industry, Chiguvi et al. (2017) confirmed a negative correlation between tangibles, assurance, responsiveness, dependability, and bank service quality. Descriptive statistics and qualitative research served as the study's foundation. Chiguvi (2016) confirmed that customer happiness and EbankQual characteristics have a high positive correlation. The research noted a low favourable association between the quality of bank services and customer loyalty. 200 FNB cell phone bank customers in Botswana were included in the descriptive study. The EBankQual model served as the foundation for the study, which evaluated how well bank service quality was affected by mobile banking.

According to Gbadeyan et al. (2015), there is a substantial and favorable correlation between the financial services quality offered by Nigerian banks and the SERQUAL dimensions. The study was based on qualitative research using a sample of 385 clients selected from Nigeria's top five banks. A convenience and purposive sampling strategy was used to choose the sample.

A national service quality index was inverted by Abdullah et al. (2011) to appraise the quality of the banking industry. According to Abdullah et al. (2011), systemization, responsiveness, and trustworthy communication are the three factors that determine how well banks provide their services. An overall weighted BSQ index of 4.0 was considered a general signal that bank clients were satisfied with the service quality offered by financial institutions, and further systemization was considered the most significant service quality dimension in the banking industry (ibid). Multiple linear regressions and factorial analysis were employed in the investigation.

Research and Methodology

Equation 1 below illustrates the regression equation, which served as the basis for the study's quantitative research technique. The study used Analysis of Moments Structures (AMOS) to perform Structural Equation Modelling (SEM) to evaluate hypotheses. This is in consistent with the research design that was applied in Zhou et al. (2021), Islam et al. (2021) and Abdullah et al. (2011). Structural equation modeling was used to create a new model, concept model A, which is displayed in Figure 4.1 below. The study used random sampling in selecting the respondents to the study. Eight hundred structured questionnaires were administered to the respondents. Karakaya-Ozyer and Aksu-Dunya (2018) alluded to choosing the right sample size as crucial SEM choice that needs to be carefully considered. For EFA, Surucu (2022) recommended a sample size of at least 400. Wolf et.al (2013) recommended a sample size of at least 100 to 200. In order to improve the validity and reliability of the findings and inferences to be made, the current study used a sample of 800.

The regression equation that represents this study is illustrated in Equation 1 below.

Equation 1: Determinants of Bank Service Quality

![]()

Rationale of using Structural Equation Modelling (SEM)

Hoyle (2015) asserted SEM is a set of analytical techniques required to represent the relationships between data items. Schumacher and Lomax (2016) acclaimed that SEM is used to statistically assess the study's proposed research hypotheses as well as the researcher's theoretical models, which often explain the relationships between latent and observable variables. Schumaker and Lomax (2016) asserted that SEM is only a tool for confirming the researcher's theoretical models. Ramsey and Schafer (2013) deduced that the variables used in SEM are linear combinations of several factors chosen to help with the study problem. SEM was therefore used in this study as it was thought to be a suitable method for dealing with the current research problem that included testing the hypothesis that bank service quality is not significantly correlated with the SERVQUAL variables of tangibles, responsiveness, reliability, empathy and assurance.

Results

The research results are presented in terms of the following subsections, demographic analysis, survey descriptive statistics, reliability analysis tests, Kaiser Meyers Olkins (KMO) sampling adequacy tests, and the results of structural equation modeling (SEM).

Demographic Analysis for the study

According to table 1 below, there were roughly 41% men and 59% women among the study's respondents. Table 2 below reveals that 41% of the study participants were between the ages of 21 and 23, 29% were between the ages of 18 and 20, 16% were between the ages of 24 and 26, and roughly 14% were between the ages of 27 and over. As indicated in Table 3 below, 61% of the respondents held a bachelor's degree, 19% a master's degree, 6% a doctorate, and the remaining 14% held a diploma, certificate, or other educational credentials below a certificate. Table 4 below illustrated that 31% of respondents had been faithful to their bank for at least three years, 24% had been devoted for one to two years, and 45% had been loyal for up to one year. As indicated in table 5 below, 38% of the clients had FNB bank accounts, 34% Standard Chartered Bank customers, 15% ABSA customers, 9% Stanbic customers, and 4% ACCESS and Bank of Gaborone customers.

Table 1: Gender

Mode | % | % Valid | % Cumulative | ||

Valid | Male | 308 | 40.0 | 40.0 | 40.0 |

Female | 452 | 58.7 | 58.7 | 98.7 | |

3 | 8 | 1.0 | 1.0 | 99.7 | |

6 | 2 | 0.3 | 0.3 | 100.0 | |

Total | 770 | 100.0 | 100.0 |

Source: Authors, 2024

Table 2: Age

Mode | % | % Valid | % Cumulative | ||

Valid | 18-20 years | 220 | 28.6 | 28.6 | 28.6 |

21-23 years | 318 | 41.3 | 41.3 | 69.9 | |

24-26 years | 120 | 15.6 | 15.6 | 85.5 | |

27-29 years | 42 | 5.5 | 5.5 | 90.9 | |

30-35 years | 32 | 4.2 | 4.2 | 95.1 | |

36-40 years | 18 | 2.3 | 2.3 | 97.4 | |

41-45 years | 10 | 1.3 | 1.3 | 98.7 | |

46-50 years | 2 | 0.3 | 0.3 | 99.0 | |

51 and above years | 8 | 1.0 | 1.0 | 100.0 | |

Total | 770 | 100.0 | 100.0 |

Source: Authors, 2024

Table 3: Qualification

Mode | % | % Valid | % Cumulative | ||

Valid | Doctorate | 42 | 5.5 | 5.5 | 5.5 |

Masters | 144 | 18.7 | 18.8 | 24.2 | |

Bachelors | 468 | 60.8 | 60.9 | 85.2 | |

Diploma | 40 | 5.2 | 5.2 | 90.4 | |

Certificate | 44 | 5.7 | 5.7 | 96.1 | |

Below certificate | 28 | 3.6 | 3.6 | 99.7 | |

9 | 2 | 0.3 | 0.3 | 100.0 | |

Total | 768 | 99.7 | 100.0 | ||

Total | 770 | 100.0 | |||

Source: Authors, 2024

Table 4: Years of Service Loyalty

% | % Valid | % Cumulative | |||

Valid | 0-3 months | 90 | 11.7 | 11.7 | 11.7 |

4-6 months | 90 | 11.7 | 11.7 | 23.4 | |

7-9 months | 60 | 7.8 | 7.8 | 31.2 | |

10-12 months | 108 | 14.0 | 14.0 | 45.2 | |

1-2years | 182 | 23.6 | 23.6 | 68.8 | |

3 years and above | 238 | 30.9 | 30.9 | 99.7 | |

7 | 2 | 0.3 | 0.3 | 100.0 | |

Total | 770 | 100.0 | 100.0 |

Source: Authors, 2024

Table 5: Bank

Mode | % | % Valid | % Cumulative | ||

Valid | FNB | 296 | 38.4 | 38.4 | 38.4 |

ABSA | 116 | 15.1 | 15.1 | 53.5 | |

STANCHART | 264 | 34.3 | 34.3 | 87.8 | |

STANBIC | 70 | 9.1 | 9.1 | 96.9 | |

ACCESS | 12 | 1.6 | 1.6 | 98.4 | |

BANK OF GABORONE | 12 | 1.6 | 1.6 | 100.0 | |

Total | 770 | 100.0 | 100.0 |

Source: Authors, 2024

Descriptive Statistics for Bank Service Quality Survey

On average at least 30% of the respondents agreed that specific bank services characteristics of the tangibles (A22-30%), reliability (A23-28%), responsiveness (A24-32%), assurance (A25-30%) and empathy (A26-30%) were the determinants of bank service quality and whist less 26% of the respondents on average strongly disagreed, as shown from table 6 to table 10 below.

Table 6: Tangibles

Mode | % | % Valid | % Cumulative | ||

Valid | Strongly Disagree | 132 | 17.1 | 17.1 | 17.1 |

Disagree | 170 | 22.1 | 22.1 | 39.2 | |

Neutral | 220 | 28.6 | 28.6 | 67.8 | |

Agree | 108 | 14.0 | 14.0 | 81.8 | |

Strongly Agree | 126 | 16.4 | 16.4 | 98.2 | |

6 | 12 | 1.6 | 1.6 | 99.7 | |

7 | 2 | 0.3 | 0.3 | 100.0 | |

Total | 770 | 100.0 | 100.0 |

Source: Authors, 2024

Table 7: Reliability

Mode | % | % Valid | % Cumulative | ||

Valid | Strongly Disagree | 176 | 22.9 | 22.9 | 22.9 |

Disagree | 184 | 23.9 | 23.9 | 46.8 | |

Neutral | 184 | 23.9 | 23.9 | 70.6 | |

Agree | 68 | 8.8 | 8.8 | 79.5 | |

Strongly Agree | 148 | 19.2 | 19.2 | 98.7 | |

6 | 6 | 0.8 | 0.8 | 99.5 | |

7 | 4 | 0.5 | 0.5 | 100.0 | |

Total | 770 | 100.0 | 100.0 |

Source: Authors, 2024

Table 8: Responsiveness

Mode | % | % Valid | % Cumulative | ||

Valid | Strongly Disagree | 194 | 25.2 | 25.2 | 25.2 |

Disagree | 176 | 22.9 | 22.9 | 48.1 | |

Neutral | 142 | 18.4 | 18.4 | 66.5 | |

Agree | 98 | 12.7 | 12.7 | 79.2 | |

Strongly Agree | 152 | 19.7 | 19.7 | 99.0 | |

6 | 8 | 1.0 | 1.0 | 100.0 | |

Total | 770 | 100.0 | 100.0 |

Source: Authors, 2024

Table 9: Assurance

Mode | % | % Valid | % Cumulative | ||

Valid | Strongly Disagree | 200 | 26.0 | 26.0 | 26.0 |

Disagree | 170 | 22.1 | 22.1 | 48.1 | |

Neutral | 160 | 20.8 | 20.8 | 68.8 | |

Agree | 86 | 11.2 | 11.2 | 80.0 | |

Strongly Agree | 146 | 19.0 | 19.0 | 99.0 | |

6 | 2 | 0.3 | 0.3 | 99.2 | |

7 | 6 | 0.8 | 0.8 | 100.0 | |

Total | 770 | 100.0 | 100.0 |

Source: Authors, 2024

Table 10: Empathy

Mode | % | % Valid | % Cumulative | ||

Valid | Strongly Disagree | 200 | 26.0 | 26.0 | 26.0 |

Disagree | 170 | 22.1 | 22.1 | 48.1 | |

Neutral | 160 | 20.8 | 20.8 | 68.8 | |

Agree | 86 | 11.2 | 11.2 | 80.0 | |

Strongly Agree | 146 | 19.0 | 19.0 | 99.0 | |

6 | 2 | 0.3 | 0.3 | 99.2 | |

7 | 6 | 0.8 | 0.8 | 100.0 | |

Total | 770 | 100.0 | 100.0 |

Source: Authors, 2024

Results of Reliability Analysis and Sampling Adequacy outcome for the Scale measurement Items

As indicated in Table 11 below, the study's scale items passed reliability testing as well as the Kaiser Meyers Olkins (KMO) and Bartlet tests, receiving scores of at least 0.7 and 0.8, respectively. Therefore, confirmatory factor analysis was conducted before Structural Equation Modelling (SEM) was applied to each of the data sets evaluating the factors influencing the quality of bank services due to the reliability analysis and KMO test findings being positive. Additionally, as seen in Table 11 below, each scale measurement item had appropriate communality values of roughly 0.7. Prior to using SEM, Surucu (2022) advised testing the data items for reliability and sample adequacy.

Although this study employed a cut off 0.5 of factor loadings to clean and ensure quality, Samuels (2016) advised a factor loading of at least 0.2 to ensure quality. As a result, the reliability and KMO test results show that the scale measurement items utilized in the study were of adequate quality.

Table 11: Results of Reliability Analysis and Sampling Adequacy for Scale Items

Scale Measurement Item | Tangible (F2) | Reliability (F3) | Responsiveness (F4) | Assurance (F5) | Empathy (F6) | Service Quality (F1) |

Cronbachâs Alpha for Reliability Analysis | 0.874 | 0.895 | 0.885 | 0.891 | 0.851 | 0.915 |

Kaiser Meyers Olkins (KMO) test for Sampling Adequacy | 0.832 | 0.859 | 0.819 | 0.821 | 0.801 | 0.862 |

Communalities | 0.700 | 0.689 | 0.733 | 0.777 | 0.674 | 0.862 |

Source: Authors, 2024

The Results of the Structural Equation Modelling (SEM) of the Study

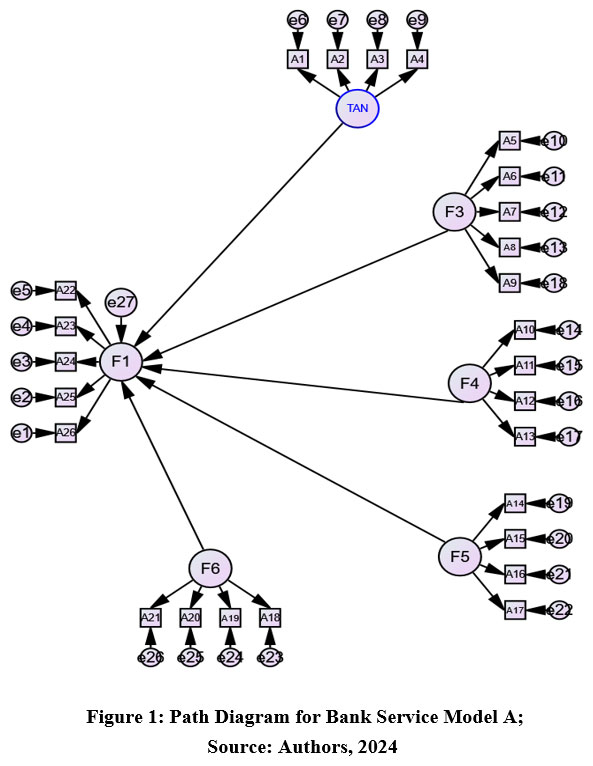

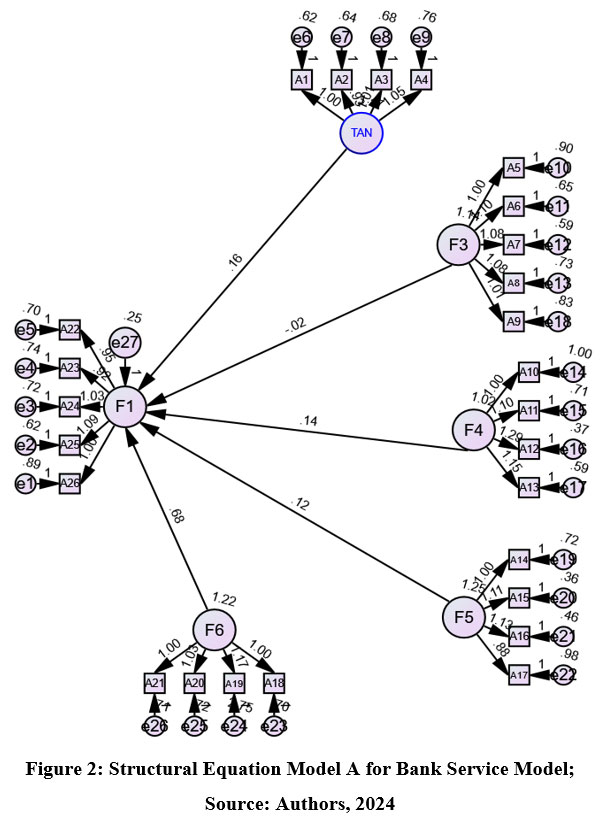

As may be seen below, the SEM results are displayed in Figure 1, Tables 12 through 14. The path diagram for structural equation concept model A, which was inverted for the investigation, is shown in Figure 1. As shown in Figure 12 below, the structural concept model A showed that tangibles (F2), responsiveness (F4), assurance (F5), and empathy (F6) had a substantial and positive correlation with bank service quality (F1). The results concured with the findings of Zhou et al. (2021), Islam et al. (2021), Dongol and Khadka (2024), Thao (2022), Chiguvi (2023) and Neupane (2019). However, the findings are in contrast with the results of Chiguvi et al. (2017). Reliability (F3) and bank service quality have a negligible and inverse relationship, according to structural equation model A. This outcome is in alignment with the research findings of Islam et al. (2021) and contrasted with findings of Gbadeyan et al. (2015) and Suzan et al. (2021). This inconclusive adverse negligible relationship between bank service quality and reliability could have been caused by mixed contrasting responses that were provided regarding reliability of bank service quality in Botswana.

| Figure 1: Path Diagram for Bank Service Model A ; Source: Authors, 2024 |

| Figure 2: Structural Equation Model A for Bank Service Model; Source: Authors, 2024

|

Model Fit Summaries

The following Tables 12, 13, 14, and 15 depicted the fitness of the variables used in the creation of the new structural equation model A. The following measures were used in assessing the fitness of the new model A, Normed Fit Index (NFI), Comparative Fit Index (CFI), Relative Fit Index (RFI), Root Mean Square Error of Approximation (RMSEA), Incremental Fit Index (IFI), Chi-square degrees of freedom and Tucker Lewis Index (TLI).

Table 12: Model Fit Summary for Structural Equation Model A

Model | NPAR | CMIN | DF | P | CMIN/DF |

Default model | 83 | 4139.188 | 294 | .000 | 14.079 |

Saturated model | 377 | .000 | 0 | ||

Independence model | 52 | 15660.398 | 325 | .000 | 48.186 |

Source: Authors

Table 13: Baseline Comparisons

Model | NFI | RFI | IFI | TLI | CFI |

Default model | .736 | .708 | .750 | .723 | .749 |

Saturated model | 1.000 | 1.000 | 1.000 | ||

Independence model | .000 | .000 | .000 | .000 | .000 |

Source: Authors

Table 14: Results of the Root Mean Square Error Approximation (RMSEA).

Model | RMSEA | LO 90 | HI 90 | PCLOSE |

Default model | .130 | .127 | .134 | .000 |

Independence model | .248 | .244 | .251 | .000 |

Table 15: Model Fit Summary for the Bank Service Concept Model

Model Fit Index | Required Result | Actual Result |

NFI | > 0.900 | 0.736 |

RFI | 0-1 | 0.708 |

IFI | > 0.900 | 0.750 |

TLI | > 0.900 | 0.726 |

CFI | > 0.900 | 0.749 |

RMSEA | <0.080 | 0.130 |

CMIN/DF | <3 | 14.0 |

Source: Authors

Discussions

A new bank service concept model A, seen in Figure 2 above, was inverted by the SEM applied in the study. The findings of the SEM test of the hypothesis showed that responsiveness, assurance, empathy, and tangible service features are all significantly and favourably correlated with the quality of bank services. This outcome concurs with general sentiments of Chiguvi et al. (2025), Alall (2024), Muchimba and Sinkala (2024), Madhushani et al. (2023), Lim et al. (2023), Wang et al. (2023), Neupane (2019) and Raza et al. (2020). This result led to the rejection of the null hypothesis. In contrast, the structural equation model A also showed that the bank services quality is inversely and negligibly correlated with reliability service characteristic. This led to inconclusive evidence as reliability is inevitably expected empirically to correlate significantly and favourably with reliability (Gbadeyan et al., 2015; Mukelabi and Mulungu, 2024; Dongol and Khadka, 2024 and Wang et al., 2023). Nevertheless, this resulted in the study's null hypothesis about the reliability of the services being accepted.

Conclusion

It can be concluded that bank service quality is profoundly and positively correlated with responsiveness, assurance, empathy, and tangible service characteristics It can also be affirmed that bank service quality is insignificantly and negatively associated with service characteristics of reliability.

Hence the inconsistency in the relationship between bank service quality and reliability raises eyebrows regarding important policy implications that need to be addressed regarding reliability issues within the banking sector of Botswana. Therefore, banks should make an effort to consistently apply reliability to all of their services, reduce needless waiting times (in lines), and get rid of some procedures and systems that don't add value towards the quality of their-services. Furthermore, banks should replace manual bottleneck activities with self-service automated systems in the banking halls to expedite reliability and further reduce time spent on queuing in the banking halls.

It is advised that banks give priority to meeting the tangible service needs of responsiveness, assurance, empathy, and tangibles without sacrificing total customer reliability to enhance customer satisfaction. Legislators should also pass laws requiring banks to offer services that encourage green finance and refrain from contributing to green washing. Lastly the direction of future discourse should be focused on the relevance of human service reliability in the wake of application of artificial intelligence (AI) towards the fulfilment of banking customer satisfaction.

Acknowledgement

The author is grateful to the Botswana Ministry of Finance for issuing us with a research permit to conduct the research in the financial markets of Botswana. No materials were reproduced but figures and tables were the result of research data that were processed through SPSS and AMOS for structural equation modeling.

Funding Sources

The authors received no financial support for the research, authorship, and/or publication of this article.

Conflict of Interest

The authors do not have any conflict of interest.

Data Availability Statement

The corresponding author can provide the data from this study upon request. Due to limitations, the data are not publicly accessible.

Ethics Statement

Testing of any material, animal subjects which required ethical approval were not part of the research. However the researchers obtained a research permit to administer the questionnaires on human subjects in the financial markets of Botswana.

Informed Consent Statement

Every participant in the study provided their informed consent.

Permission to reproduce material from other sources

Not Applicable

Author Contributions:

Wilbert Kudakwashe Chidaushe: WritingâReview and Editing, Conceptualization, Methodology, and Resources

Stegi Shine: WritingâOriginal Draft, WritingâReview and Editing, Validation, Formal Analysis.

Mini Sebastian: WritingâReview and Editing, Methodology, Formal Analysis, Investigation

References

- Abdullah, F., Suhaimi, R., Saban, G. and Hamali, J. (2011), "Bank Service Quality (BSQ) Index: An indicator of service performance", International Journal of Quality & Reliability Management, Vol. 28 No. 5, pp. 542-555. https://doi.org/10.1108/02656711111132571.

CrossRef - Alall, H.A.E. (2024). The Impact of Quality of Banking Services on the Customer Satisfaction in Small and Medium Banks. Vol. 5 No. 2 (2024): South Asian Journal of Social Sciences and Humanities Vol. 5(2), pp.35-44. https://doi.org/10.48165/sajssh.2024.5.2.03

CrossRef - Awara, N.F., Anyadighibe, J. A., and Bassey, F. O. (2022). Service Quality and Customer Satisfaction of Banking Services in Nigeria. African Journal of Business and Economic Research, Vol. 17(4). https://hdl.handle.net/10520/ejc-aa_ajber_v17_n4_a12

CrossRef - Bala, T. , Jahan, I. , Amin, M. , Tanin, M. , Islam, M. , Rahman, M. and Khatun, T. (2021). Service Quality and Customer Satisfaction of Mobile Banking during COVID-19 Lockdown; Evidence from Rural Area of Bangladesh. Open Journal of Business and Management, Vol 9(5), pp. 2329-2357. doi: 10.4236/ojbm.2021.95126. https://www.scirp.org/journal/paperinformation?paperid=111958

CrossRef - Chiguvi, D., Tadu, R., and Mugwati, M. (2025). Customer Experience Management in the Banking Sector and Its Relation to the SDGs. Journal of Lifestyle and SDGs Review, 5(2), e03772. https://doi.org/10.47172/2965-730X.SDGsReview.v5.n02.pe03772

CrossRef - Chiguvi, D. (2023). Analysis of the effectiveness of e-customer service platforms on customer satisfaction at ABSA, Botswana. International Journal of Research in Business and Social Science. Vol 12 (1). https://www.ssbfnet.com/ojs/index.php/ijrbs/article/view/2283.

CrossRef - Chiguvi, D., Muchingami, L., and Chuma, R. (2017). A Study on Customer Satisfaction in Commercial Banks in Botswana. International Journal of Innovative Research in Science, Engineering and Technology. Vol 6 (4). https://www.ijirset.com/upload/2017/april/2_A%20STUDY.pdf

- Chiguvi, D. (2016). Effectiveness of Cellphone Banking on Service Quality in Commercial Banks in Botswana. International Journal of Science and Research. Vol5(8). https://api.semanticscholar.org/CorpusID:34970014

- Christanto, Y. M., and Santoso, S. (2022). The influence of service quality, corporate image, and customer satisfaction on customer loyalty in banking sector in Yogyakarta. International Journal of Research in Business and Social Science (2147- 4478), 11(7), 09â16. https://doi.org/10.20525/ijrbs.v11i7.2025

CrossRef - Das, S. and Jannat, F. (2018). Impact of Service Quality on Customers' Satisfaction: An Empirical Study on State-Owned Commercial Banks in Bangladesh. Dhaka University Journal of Management, Vol. 12( 2), https://ssrn.com/abstract=4972618 or http://dx.doi.org/10.2139/ssrn.4972618

CrossRef - Desklib (2021). A study on the dimensions of service quality in the banking sector and its effect on customer satisfaction. Date accessed 02 January 2025. https://desklib.com/document/abstract-service-quality-in-the-banking/

- Dongol, P., and Khadka, S. (2024). Determinants of customer satisfaction in Nepalese banking sector. Nepal journal online.Sadgamaya vol 1(1), pp.12-16. ISSN-3021-9566. https//www.nepjol.info.

CrossRef - Famiyeh, S., Asante-Darko, D. and Kwarteng, A. (2018). Service quality, customer satisfaction, and loyalty in the banking sector: The moderating role of organizational culture. International Journal of Quality & Reliability Management, Vol 35(8), pp. 1546-1567. https://doi.org/10.1108/IJQRM-01-2017-0008

CrossRef - Feng, L., Hui, L., Meiqian,H., Kangle, C., and Mehdi, D. (2021). Customer satisfaction with bank services: The role of cloud services, security, e-learning and service quality. Technology in Society, Elsevier, vol. 64(C). https://ideas.repec.org/a/eee/teinso/v64y2021ics0160791x20312902.html

- Gbadeyan, R. A., Adeoti, J. O., and Adebisi, A.O. (2015). Bank Service Quality and Customersâ Patronage in selected banks in Southwestern Nigeria. Botswana Journal of Business. Vol 8 (1). https://journals.ub.bw/index.php/bjb/article/view/476.

- Gonu, E., Agyei, P.M., Richard, O. K., Asare-Larbi, M. (2022). Customer orientation, service quality and customer satisfaction interplay in the banking sector: An emerging market perspective. Cogent Business and Management. Vol 10 (1). https://doi.org/10.1080/23311975.2022.2163797

CrossRef - Hoyle, R.H. (2015). Introduction and overview. (In Hoyle, R.H. ed. Handbook of structural equation modelling. 1st ed. New York: The Guilford Press. p. 3-16). https://pdfcoffee.com/handbook-of-structural-equation-modeling-hoyle-pdf-free.html

CrossRef - Ifedi, C., Haque, R.,Senathirajah, A. R. B. S. and Qaz,S.Z.(2024). Service quality influence on consumer satisfaction in the banking sector aimed at sustainability growth. RGSA âRevista de Gestão Social e Ambiental. DOI: https://doi.org/10.24857/rgsa.v18n7-032. https://rgsa.openaccesspublications.org/rgsa/article/view/6025/2291

CrossRef - Islam, R., Ahmed, S., Rahman, M., and Asheq, A.A. (2021). Determinants of Service Quality and its effect on Customer Satisfaction: An Empirical Study of the Banking Sector. The TQM journal, Vol 33 (6), pp1163-1182. https://www.emerald.com/insight/content/doi/10.1108/TQM-05-2020-0119/full/html

CrossRef - Jefferis, K. (2015). Enhancing access to banking and financial services in Botswana. https://econsult.co.bw/tempex/Access%20to%20Finance%20Botswana(4).pdf. Accessed on 09 September 2024.

- Karakaya-Ozyer, K. & Aksu-Dunya, B. (2018). A review of structural equation modelling applications in Turkish educational science literature, International Journal of Research in Education and Science (IJRES), 4(1):279-291. https://www.scirp.org/reference/referencespapers?referenceid=3043653.

CrossRef - Khan, A. G., Reshma Pervin Lima, R. P., and Mahmud,S. Md. (2018). Understanding the Service Quality and Customer Satisfaction of Mobile Banking in Bangladesh: Using a Structural Equation Model. Vol 22(1), pp.109-209.https://doi.org/10.1177/0972150918795551.

CrossRef - Lim, K.B.,Yeo, S. F., Tey, Y. N., and Tan, C. L.(2023). Customer Satisfaction on E-Banking Service Quality In Malaysia. International Journal of Entrepreneurship, Business and Creative Economy, Vol. 3(2) https://doi.org/10.31098/ijebce.v3i2.1333

CrossRef - Madhushani, W.A.I. and Rajapaksha, R.L.P.W. and Dilshani, U.P. and Abeyrathne, G.R.H.S. and Weligodapola, M. and Dunuwila, D.V.R. (2023).

- The Relationship between Service Quality and Customer Satisfaction in Sri Lankan Banks. Proceedings of 13th International Conference on Business & Information (ICBI) 2022. https://ssrn.com/abstract=4453720 or http://dx.doi.org/10.2139/ssrn.4453720

CrossRef - Monosimanegape, P., Jaiyeoba, O., and Cheneso, C. H. (2020). Examining the Relationship between Service Quality and Customer Satisfaction in the Public Service. The Case of Botswana. https://api.semanticscholar.org/CorpusID:2212954

CrossRef - Muchimba, C. M., & Sinkala, M. . (2024). An Investigation of the Effect of Service Quality on Customer Satisfaction: A Case of Zanaco Bank. African Journal of Commercial Studies, 4(3), pp.178-185. https://doi.org/10.59413/ajocs/v4.i3.1

CrossRef - Mukelabai , N., & Mulungu, C. (2024). Impact of Quality Service Delivery Challenges on Customer Satisfaction in the Banking Industry: A Case of Stanbic Bank, Zambia. International Journal of Business, Management and Economics, 5(2), pp.134 - 154. https://doi.org/10.47747/ijbme.v5i2.1767

CrossRef - Neupane, R. (2019). Determinants of Customer Satisfaction of Public Banks in Nepal. International Journal of Management and Humanities (IJMH) ISSN: 2394-0913, (Online), Vol 3(11). https://www.ijmh.org/wp-content/uploads/papers/v3i11/K02960731119.pdf

CrossRef - Parasuraman, A., Zeithami, V. A., & Berry, L. L. (1988). SERVQUAL: A multiple-item scale for measuring consumer perceptions of service quality. Journal of Retailing, 64(1), 12â40. https://psycnet.apa.org/record/1989-10632-001.

- Patel, R., Mishra, A. K., Chishti, M. Z., and Mod, T. M. (2023). Relationship Between Internet Banking Service Quality, e-Customer Satisfaction, and Loyalty: A Comparative Study of India and Pakistan. Journal of Central Banking Theory and Practice, Vol 13(2), pp. 213-228. DOI: 10.2478/jcbtp-2024-0019. https://www.cbcg.me/slike_i_fajlovi/fajlovi/journal/vol13/jcbtp-2024-0019.pdf.

CrossRef - Raza, S. A., Umer, A., Qureshi, M.A., and Dahri,A.S. (2020). Internet banking service quality, e-customer satisfaction and loyalty: the modified e-SERVQUAL model. The TQM Journal, Vol. 32(6), pp. 1443-1466. https://doi.org/10.1108/TQM-02-2020-0019. https://www.emerald.com/insight/content/doi/10.1108/tqm-02-2020-0019/full/html

CrossRef - Ramsey, F. & Schafer, D. (2013). The statistical sleuth: A course in methods of Data-analysis.-3rd-ed.-Boston:-Cengage-Learning. https://bridge.primo.exlibrisgroup.com/discovery/fulldisplay/alma991001891919702971/01BRC_INST:CCO

- Samuels, P. (2016). Advice-on-exploratory factor-analysis. https://www.researchgate.net/publication/304490328_ Advice_on_Exploratory_ Factor_Analysis.

- Schumacher, R.E. & Lomax, R.G. (2016). A beginnerâs guide to structural Equation-modeling.-4th-ed.-New-York:-Routledge. https://www.scirp.org/reference/referencespapers?referenceid=2501955

- Singh, S. (2019). Measuring E-Service Quality and Customer Satisfaction with Internet Banking in India. Theoretical economic letters, Vol 9 (2), pp.308-326. doi: 10.4236/tel.2019.92023. https://www.scirp.org/journal/paperinformation?paperid=90689

CrossRef - Siregar, R. G. V., and Kusumawati, N. (2023). Investigating the Impact of Service Quality on Customer Satisfaction and Subsequent Customer Loyalty in Bank Jago. Journal Integration of Management Studies, 1(2), 194â202. https://doi.org/10.58229/jims.v1i2.113

CrossRef - Surucu, L. (2022). Exploratory Factor Analysis (EFA) in Quantitative Research and Practical Considerations. DOI: 10.31219/osf.io/fgd4e ORCID ID: https://orcid.org/0000-0002-6286-4184. https://ideas.repec.org/p/osf/osfxxx/fgd4e.html.

- Suzan, M., Winarto, J., and Gunawan, I. (2021). Development of service quality model as determinants toward banking performance. Studies of applied economics, vol 39(4). https://doi.org/10.25115/eea.v39i4.4629. https://ojs.ual.es/ojs/index.php/eea/article/view/4629

CrossRef - Thao, P.T. X. (2022). Factors driving customer satisfaction in Vietnbankâ retail banking product. Journal of Finance-marketing, Vol 72(6), pp.117-126. DOI: https://doi.org/10.52932/jfm.vi72.

CrossRef - Tedjokusumo, C. and Murhadi, W.R. (2023). Customer satisfaction as a mediator between service quality and customer loyalty: a case study of Bank Central. Journal Siasat Bisnis, Vol.27(2), pp,156â170. https://doi.org/10.20885/jsb.vol27.iss2.art3

CrossRef - Wang, C.K., Masukujjaman, M., Alam, S.S., Ahmad, I., Lin, C.Y and Ho, Y.H. (2023). The Effects of Service Quality Performance on Customer Satisfaction for Non-Banking Financial Institutions in an Emerging Economy. Int. J. Financial Stud. 2023, 11(1), 33; https://doi.org/10.3390/ijfs11010033

CrossRef - Wolf, E.J., Harrington, K.M., Clark, S.L. & Miller, M.W. (2013). Sample size requirements for structural equation models: An evaluation of power, bias, and solution. Propriety Educ Psychol Meas, 76(6):913â934. https://pubmed.ncbi.nlm.nih.gov/25705052/

CrossRef - Vinnarasi B, Kumar, N., Ganesh, Ch., Agarwal, A. and Maguluri,L.P. (2022). Service quality and customer satisfaction with special reference to banking sector. Journal of positive school psychology, Vol 6 (5), pp.1477-1485. http://journalppw.com.

- Zhou, Q. Lim, F.L., Yu, H., Xu.G., Ren,X., Liu, D., Wang, X., Mai. X. and Xu, H. (2021). A study on factors affecting service quality and loyalty intention in mobile banking. Journal of Retailing and Consumer Services, Vol 60. https://doi.org/10.1016/j.jretconser.2020.102424.

CrossRef

JSE Classification: G21, C02, C120, Q5

This work is licensed under a Creative Commons Attribution 4.0 International License.